David Beckworth—Monetary Policy at the Zero Lower Bound: 3 Quasi-Natural Experiments

Link to the post on David Beckworth's Macro and Other Market Musings blog

I appreciate David giving me permission to reprint his post here.

Can monetary policy still pack a punch at the zero lower bound (ZLB)? For Market Monetarists, the answer is an unequivocal yes. For others, the answer is less clear. Paul Krugman, for example, made the following comment recently on the efficacy of monetary policy during liquidity traps:

[T]he liquidity trap is real; conventional monetary policy, it turns out, can’t deal with really large negative shocks to demand. We can argue endlessly about whether unconventional monetary policy could do the trick, if only the Fed did it on a truly huge scale..

Krugman is right, this issue is contentious. It has been argued almost endlessly over the past five years. I submit, however, that over this time we have had several quasi-natural experiments on the effectiveness of monetary policy at the ZLB. These “experiments” along with an earlier one have shed some light on this issue.

1. The first quasi-natural experiment has been happening over the course of this year. It is based on the observation that monetary policy is being tried to varying degrees among the three largest economies in the world. Specifically, monetary policy in Japan has been more aggressive than in the United States which, in turn, has had more aggressive monetary policy than the Eurozone.

These economies also have short-term interest rates near zero percent. This makes for a great experiment on the efficacy of monetary policy at the ZLB.

So what have these monetary policy differences yielded? The chart at the top answers the question in terms of real GDP growth through the first half of 2013.

The outcome seems very clear: when really tried, monetary policy can be very effective at the ZLB. Now fiscal policy is at work too, but for this period the main policy change in Japan has been monetary policy. And according to the IMF Fiscal Monitor, the tightening of fiscal policy over 2013 has been sharper in the United States than in the Eurozone. Yichang Wang illustrates this latter point nicely in this figure. So that leaves the variation in real GDP growth being closely tied to the variation in monetary policy. Chalk one up for the efficacy of monetary policy at the ZLB.

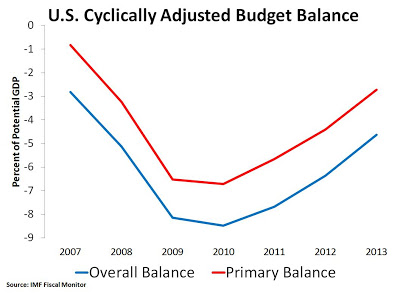

2. The second quasi-natural experiment has been running since 2010 in the United States. Over this period the cyclically-adjusted or structural budget balance as a percent of potential GDP has been shrinking. This is the best measure of the stance of fiscal policy, as noted by Paul Krugman:

[M]easuring austerity is tricky. You can’t just use budget surpluses or deficits, because these are affected by the state of the economy. You can — and I often have — use “cyclically adjusted” budget balances, which are supposed to take account of this effect. This is better; however, these numbers depend on estimates of potential output, which themselves seem to be affected by business cycle developments. So the best measure, arguably, would look directly at policy changes. And it turns out that the IMF Fiscal Monitor provides us with those estimates, as a share of potential GDP…

Below is the IMF’s measure of both the overall and primary structural budget balance for all levels of government:

So what is the implication of this figure? First, it shows that independent of business cycle influences fiscal policy has been tightening since 2010. It has gone from an overall deficit of 8.5% in 2010 to an expected one of about 4.6% in 2013. Stated differently, the above reduction in the general budget deficit is not the government endogenously adjusting its balance sheet in response to improvements in the private sector’s balance sheet. Rather, it is the consequence of explicit policy choices to sharply tighten fiscal policy.

So what have these three years of fiscal policy tightening done to aggregate demand over this time? Apparently nothing as seen in the figure below:

So what explains this development? How is it that fiscal policy tightening in conjunction with the Eurozone shocks, the China slowdown shocks, and other negative shocks has not slowed down aggregate demand growth? The answer is that Fed policy has effectively offset the effect of the fiscal austerity and the other shocks. This is another great quasi-natural experiment that demonstrates the effectiveness of monetary policy even with interest rates close to zero percent. Chalk another one up for the efficacy of monetary policy at the ZLB.

Of course, this remarkable stabilization of U.S. aggregate demand growth by the Fed has been far from adequate in terms of restoring full employment. It is, therefore, ultimately frustrating to watch. For it speaks to both the power and shortcomings of current Fed policy

3. While these recent quasi-natural experiments on the efficacy of monetary policy at the ZLB are informative, an even more telling one can be found in the 1930s. This is the quasi-natural experiment of advanced economies going off the gold standard. As is well known, the interwar gold standard was flawed and played a key role in causing the Great Depression in the early 1930s. The countries involved were in a slump and their interest rates were near zero percent. Yet, as Eichengreen (1992) notes, the quicker a country abandoned the gold standard the quicker it experienced a robust recovery.

{kind=link}

This cross-country, quasi-natural experiment of the efficacy of monetary policy at the ZLB should give any monetary skeptic pause. Christina Romer notes that in the case of the U.S. economy this recovery was almost entirely the consequence of easing monetary conditions. Fiscal policy played little role.

These three quasi-natural experiments indicate that there is much monetary policy can do at the ZLB. If so, the key issue is why central banks did not do more over the past three years to shore up the recovery.

Footnote: In more precise terms, the Bank of Japan has signaled more definitely than the Federal Reserve a permanently higher future monetary base level relative to the expected real demand for it. The Fed, in turn, has signaled the same relative to the ECB.